The narrative just changed, but so too did the mise en scene (twice!)

Inflation—runaway from its “transitory” narrative: It looks like inflation is running hotter and longer than most experts anticipated, especially in the US. The supply problem shows very few signs of fading. And price increases are intensifying.

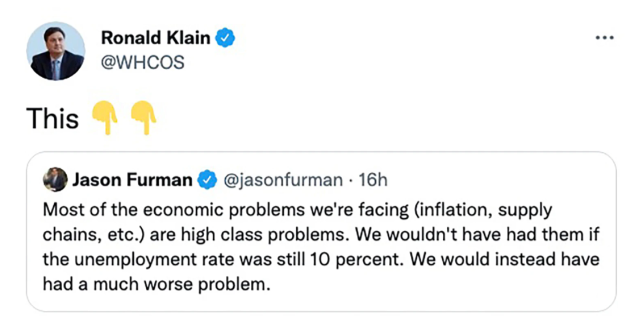

It’s an “everybody” problem: People across the globe will experience inflation differently. You can’t place it under some categorical umbrella, as WHCIF Rondald Klain did, retweeting Harvard economist Jason Furman, calling it a “high class problem.”

When you can’t locate items on the grocery shelves because they’ve run bare, it’s an “every-person” problem. When grocery prices lighten your money stash or clean you out, “class” doesn’t matter.

A monetary and political wrench: Markets hate uncertainty. That’s what narratives are for. They provide a backdrop, conflict, and resolution—all before it happens! But the inflationary scenario’s changing. And that will affect central banks’ and government fiscal policy actions (and stories), possibly all over the globe.

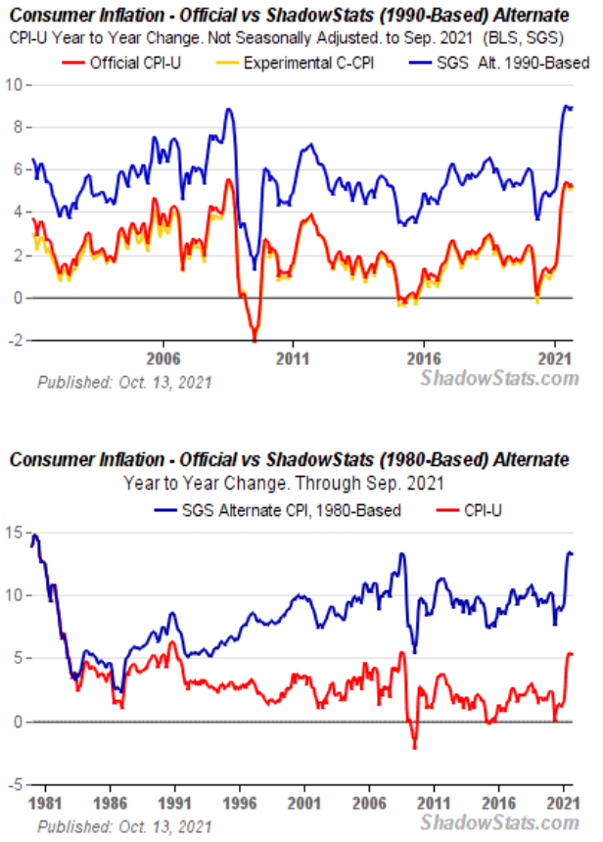

The official numbers: Current inflation rate in the US shows a significant spike to 5.4%, something we haven’t seen since 2008.

The unofficial numbers: Here’s something to ponder; an interesting piece of info that many people don’t know about: US inflation calculations have seen significant tweaks in 1980 and 1990.

So, what would happen if we were to view inflation the way we calculated it in those decades?

Whether you agree with this thesis or not, it’s worth viewing:

Economic News Watch

Regarding inflation, watch out for Australia’s CPI data on Monday, the ECB interest rate decision on Thursday, and Eurozone CPI on Friday. The big report in the US takes place on Thursday, as Q3 GDP is expected to be released.

Pure-Play Green Sentiment Waning

Price reflects the market’s price expectations based on either fundamentals, sentiment, or both combined. Since fundamentals can take months to “validate” price, we can say it reflects sentiment, one way or another.

Looking at the energy landscape through a market’s lens, we see H2O, the California Water Index futures in the midst of a drought and a dry La Nina season. XLE, representing legacy gas and oil companies, has broken through resistance to become the top market performer, reflecting optimism in legacy energy versus their green counterparts. CRBN, which tracks mainstream companies looking to cut their carbon emissions, is moving steadily but making no significant strides, as their earnings belong to their respective sectors. And the poorest performer: PBD, the Invesco Global Clean Energy fund, which provides a pure play to renewable energy companies across the globe. Pessimism toward global green policy, or an opportunity to be the “money smart” while the mainstream follows the cash?