Evergrande’s $305 billion default threat slammed the market until investors quickly forgot about it. Evergrande’s debt load of $305 billion is only half the size of now-defunct Lehman Brothers. However, its default would still be one of the largest in history. Yet, the market jitters it caused in the middle of last week was still arguably small relative to its significance.

The markets’ recovery may be due to Evergrande’s recent announcement that it will begin making payments on some of its debt. Beijing also hinted that it might allow the beleaguered construction behemoth to fail, but namely for debts held by foreign investors (that’s us, by the way, and everyone else outside of China).

What’s interesting is how quickly the market recovered by the end of the week, nearly as fast as it fell, as all eyes turned to the US Federal Reserve; the central bank is keeping interest rates unchanged while giving no timeline nor showing any urgency to take away the stimulus punch bowl. So, the party’s been extended, at least in the eyes of investors.

However, as professional market participants, you know not to take active and short-term “forgetting” as an intermediate or long-term market forecast. The background (read: ground) has a way of rushing at you, especially if you find yourself to be the one speeding to meet it from great heights.

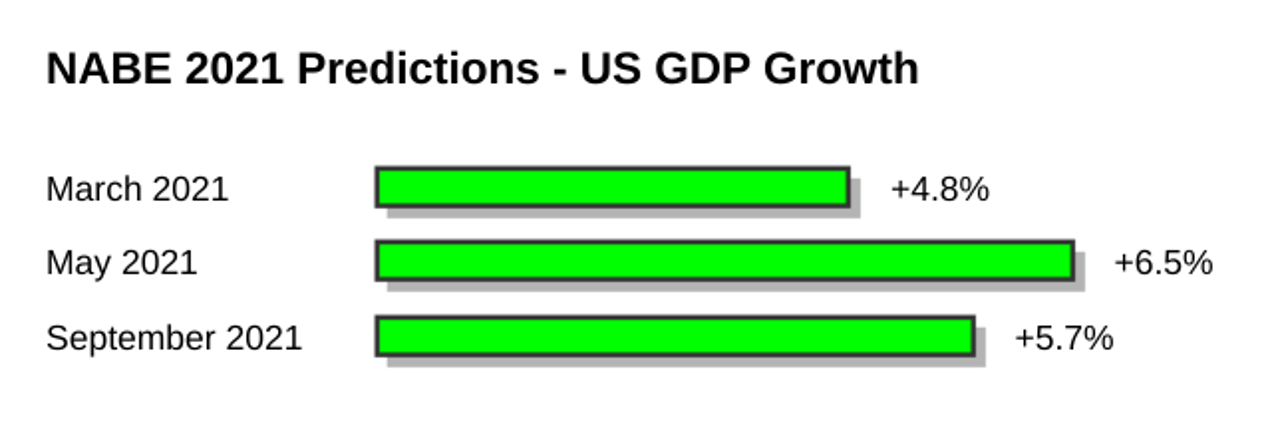

This week, markets opened up mixed, with US 10-year yields topping 1.5% for the first time since June. Anticipating Thursday’s US GDP report, business economists have tempered their 2021 growth expectations, according to the National Association for Business Economics (NABE). Expectations have fallen from +6.5% in the May survey to +5.7%. Most economists polled expect inflation to rise sharply in 2021 and moderately in 2022.

Why’s this so important? It shows that business leaders are still worried about the pandemic—namely, the Delta variant’s rapid spread. As the saying goes, “it ain’t over til it’s over,” and though the markets may be saying one thing, we can all see the big infected elephant in the room. Not surprisingly, the panellists mentioned that faster vaccine rollouts might ameliorate their general outlooks.

Economic News Watch

We’re in the last week of the quarter. ECB President Christine Lagarde speaks every day this week except Thursday when the US GDP data is slated to be released, and Federal Reserve Chair Jerome Powell chimes in on Wednesday to either elevate or crash the party.

Eurozone CPI data gets released on Friday and the US Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) Report, both of which can paint a clear near-term picture of inflation on both continents, respectively consumers and producers.

Greyness and Shine

Silver’s in a strange spot. A monetary and industrial metal hybrid, one can imagine how one set of investors might load up on the grey metal when economic growth whos signs of slowing, dumping their holdings when things improve, while another set of investors will load up on the metal when the economy emerges from a slump, dumping their holdings when times get bad. Its status and what it symbolizes is just as ambiguous as its colour—an ironic tinge of lustrous grey or a greyed lustre (depending on how you look at it).

Silver futures’ (SI) are well into their 13th-month drunk walk leading downward. Not a good prospect for investors with a myopic view. From a position trader’s lens, however, it’s not so bad. The metal hasn’t even retraced 50% of its entire move up from its March 2020 pandemic low. The metal can go as low as a 61.8% retracement—between $18 to $20 an ounce—before gold and silver bugs begin feeling their metals to be a bit “heavy.” So, the trend, ironically, is down in the short-term, sideways in the intermediate-term, and up in the long-term. Directionally speaking, that’s fuzzy grey.